2/27/2019

Is your Company in our Directory?

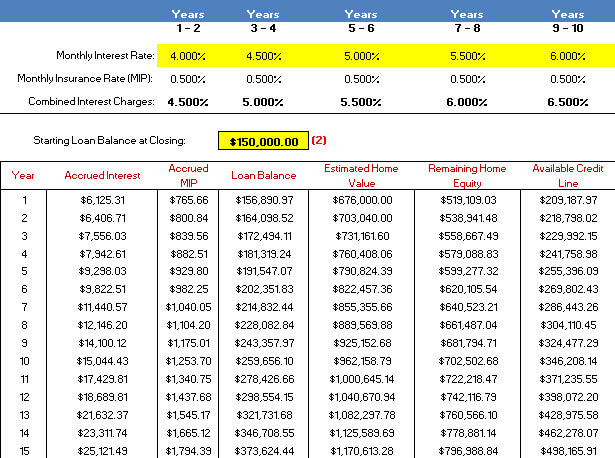

Reverse Mortgage Amortization Calculator with Free Excel Download

12/24/2018

Have you ever wondered about how a reverse mortgage loan could be more advantageous than a traditional loan? Are you someone who thinks Reverse Mortgage loans are only for those in dire straits? Think that if you get a Reverse Mortgage loan that you will have no equity in your home for the rest of your life?

I have some news for you that will make you reconsider that position and see how a Reverse Mortgage loan could be more beneficial to you than a Conventional or Standard loan.

One feature of the Reverse Mortgage loan that is not as well known as it should be is that Reverse Mortgage loans have no prepayment penalties and homeowners can make payments on these loans. That is right, you can take out a Reverse Mortgage loan that requires no monthly payments, but still make payments on the loan in order to lower the balance for the future or pay it off over a set period of time.

Since Reverse Mortgage loans do not require payment in full in order to satisfy the loan or bring down the balance, homeowners can opt to make partial repayments to the loan in a number of different ways. Some people have decided that they were going to pay just enough per month in order to keep the balance exactly the same as the amount that was borrowed at closing and others decide that they wish to pay more as they eventually want to pay the loan off.

Now one might ask “Why would I get a Reverse Mortgage loan if I am just going to make payments?” There are many reasons why people across the country are going this route. Reverse Mortgage loans are much easier to qualify for than Conventional loans as it pertains to income and credit requirements.

Those on a fixed income or those who cannot verify their income in the traditional sense may not qualify for a Conventional loan. However, since the guidelines on Reverse Mortgages currently do not require any income requirements and the credit guidelines are very minimal, it is easier to qualify for this product. However, in my opinion, the best reason why this is a more attractive option is that you are not required to make monthly payments on a Reverse Mortgage.

Since there is no requirement of payment, you can decide how much you would like to pay on a monthly basis and if a month were to come along where you could not afford to pay as much as you normally would, you could forego making a payment altogether.

This is a huge advantage over getting a traditional loan. If you could not make your full scheduled monthly payment on your traditional loan, your lender would consider you late and then it would ultimately affect your credit rating and if you could not catch up could lead to a foreclosure on the property.

The other knock about going the route of the Reverse Mortgage over the Conventional loan in some people’s opinions is that Reverse Mortgages are too expensive. The only reason why Reverse Mortgage loans were more expensive than Conventional loans are because they are FHA insured loans that require Up-front Mortgage Insurance Premiums or (UFMIP).

This is something that any FHA loan (Reverse or Forward) has. However, with the introduction of the Reverse Mortgage Saver Program, this is no longer the case. FHA released the Saver product to reduce closing costs to borrowers.

This means that borrowers who do not need to borrow the full amount that can be had on the Standard Reverse Mortgage product can opt for the Saver program and the UFMIP is reduced drastically from 2% of the property value to 0.01% of the property value and often times the Lender will credit this cost to you effectively making your cost of UFMIP zero.

This only leaves the standard 3rd party closing costs for Appraisal, Escrow, Title, etc. which would be prevalent in any loan transaction Reverse or Conventional.

Now you may be wondering “How much would I have to pay on my scenario in order to pay down the Reverse Mortgage over time if I were to get one?” All Reverse Mortgage has developed the first-ever reverse mortgage amortization calculator that allows you to do just that. You can decide how much you would want to pay on a monthly basis and the calculator can show you how that will change the amortization of your loan.

Article Source: https://reverse.mortgage/amortization-calculator

Additional Source: https://www.hud.gov/topics/information_for_senior_citizens

Other articles and publications:

All Reverse Mortgage® is proud to be Arizona's #1 Rated Reverse Mortgage Lender by the BBB with a Perfect 5.0 Stars and A+ Exemplary Rating. We currently lend in 16 states including all of Arizona.

We are proud to be Texas's #1 rated reverse mortgage lender by the BBB with a Perfect 5.0 stars and A+ review.

2/27/2019

Business details

- +1 (800) 565-1722

- 2019 W Chapman Ave

- reverse.mortgage

All Reverse Mortgage is committed to being your reverse mortgage lender because you deserve the best at the lowest price possible.

New York

company, product and service directory

company, product and service directory

Business Network 2008-2026

All rights reserved

All rights reserved